Management encourages employee social and recreational programs. These programs help ensure the mental and physical well-being of personnel and assist in recruiting and retaining employees.

It is Postal Service policy to provide equal employment opportunity for everyone, without regard to:

- Race, color, sex (including pregnancy, sexual orientation, and gender identity, including transgender status), national origin, religion, age (40 and above), genetic information, disability, or retaliation for engaging in EEO-protected activity as provided by law; or

- Other non-meritorious factors, such as political affiliation; marital status; status as a parent; and past, present, or future military service.

This policy applies to all employment matters, including but not limited to, recruitment, hiring, assignments, promotions, transfers, benefits, and discipline. Such discrimination is thus prohibited in employee social and recreational programs.

The installation head organizes and chairs the committee. To ensure that all employees are fairly represented, the balance of the committee includes a representative from each craft designated by the unions representing those crafts, and a member from supervision designated by the organization representing the supervisory employees.

An employee social and recreational committee must be established in each installation where employees receive income from vending machines or other enterprises. This committee may not have management responsibilities for such vending operations.

Members of the employee social and recreational committee must be permitted by their supervisor to attend committee meetings called by the chairperson. They must also be permitted to perform duties relating to functions of the committee while on the clock, subject at all times to the needs of the Postal Service.

The employee social and recreational committee represents all employees in the installation. It is responsible for administering social and recreational funds and administering programs for the benefit of all employees in the installation. The committee is specifically responsible for:

- Receiving, safeguarding, disbursing, and accounting for employee social and recreational funds.

- Developing and publicizing well-rounded social and recreational programs that contribute to the benefit of all employees. No single individual, group, or organization may be permitted to:

- Attach its name as a sponsor of an activity or event financed and sponsored by the social and recreational fund.

- Use such events in any way for the furtherance of its organizational objectives.

- Expending employee social and recreational funds for the social and recreational activities of all employees. No monies may accrue to the benefit of a single group, organization, or individual.

- Publishing annually the financial status of the employee social and recreational fund for the information of all employees.

- Advising the food service officer about the manner in which the vending operation in work areas is meeting employee needs and about pricing policies that should be established on vended items.

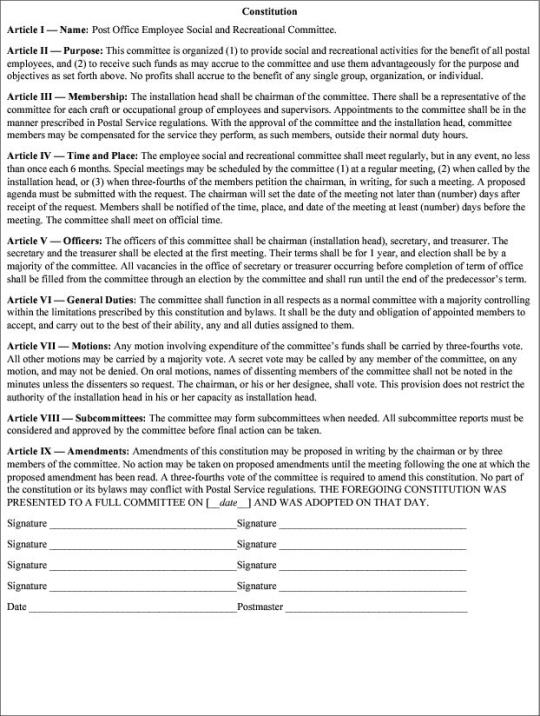

Employee social and recreational committees must operate within the framework of a constitution prepared by the committee and approved by the installation head (see Exhibit 615.34). The committee may modify the sample format to meet local conditions; however, the constitution must require that:

- The committee operations comply with applicable Postal Service rules and regulations.

- The expenditure of funds of the social and recreational committee are by a three–fourths vote.

- The accounting and auditing of all funds are as prescribed in these instructions.

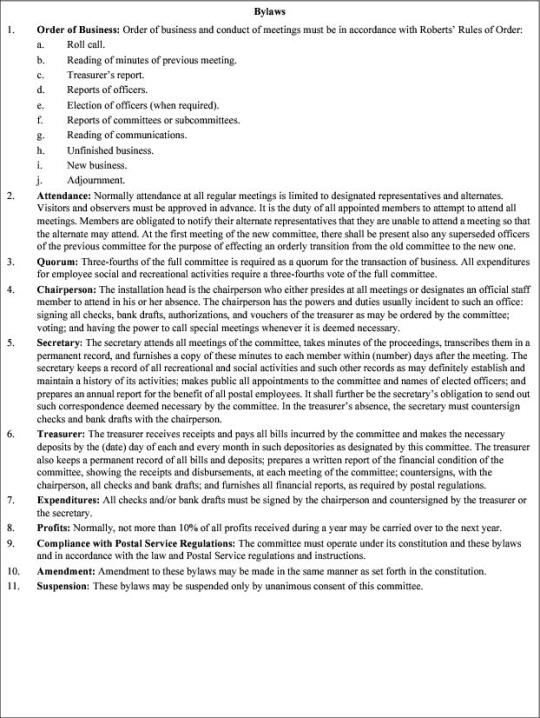

Employee social and recreational committees must operate under bylaws prepared by the committee and approved by the installation head. (See Exhibit 615.35 for a sample of bylaws.)

Exhibit 615.34

Sample Constitution

Exhibit 615.35

Sample Bylaws

The fund provides a financial basis for the support of well-rounded social and recreational programs that benefit all employees of the installation.

Funds may be derived from the following sources:

- Sale of nonalcoholic beverages, candy, cigarettes, and other consumable products by vending machines located in work areas under the following conditions:

- Employee committees may not operate vending facilities. (See Handbook EL–602, Food Service Operations, for exception.)

- The Postal Service contracts for vending services except for those operated under permit by the blind.

- Vending commissions are paid directly to the Postal Service except for income provided by the Postal Service to a state licensing agency for blind vendors under the Randolph–Sheppard Act.

- Interest on savings accounts and other investments in U.S. Savings Bonds or other securities.

- Proceeds from the sale to employees of tickets to dinners, picnics, parties, recreational activities, and discount merchandise and travel.

Monies received from the following operations are not employee social and recreational funds and are not to be included in the records or reports:

- Stands or vending machines operated by blind persons under permit.

- Funds from the operation of a cafeteria or lunchroom, including income from vending machines located in the operating areas of these eating facilities.

- Coffee shared by a group of employees on a nonprofit basis.

- Honor systems where the money received covers only the cost of the items available.

- Voluntary contributions such as those incident to the death or illness of fellow workers.

- Donations of gifts from any source. These are in violation of the Code of Ethical Conduct (see 660) and may not be accepted under any circumstances.

- Proceeds from recycling projects.

The sponsorship of insurance programs, relief or assistance funds, hardship loans, etc., are prohibited as a social and recreational program activity. Solicitations to supplement amounts contributed, or made available from the employee social and recreational fund, may not be conducted on on–the–clock time, nor may any amounts collected be included in committee fund records and reports.

One committee member should maintain the records and another committee member handle the funds when the amount of money involved warrants such division of duties.

The employee social and recreational committee is responsible for the proper safeguarding of employee social and recreational funds. All funds received throughout a postal installation must be turned over to the employee designated to handle such funds. Only one fund may be maintained for each postal installation. Separate funds may not be maintained by stations or branches.

When the average balance of a fund is less than $100, the employee social and recreational committee decides whether to maintain a bank or credit union account. Funds not deposited in a bank or other savings institution must be given the best protection available so that unauthorized persons do not have access to them. Normally, a safe should be used.

When the average balance of a fund is $100 or more, all funds, except those retained as petty cash, must be deposited in a bank or credit union. Deposits should be made as frequently as necessary consistent with the type and amount of funds received.

No more than one checking account should be maintained without the approval of the district Finance manager. Checking accounts must be carried in commercial banks insured by the Federal Deposit Insurance Corporation unless no such insured bank is available locally. The balance in a checking account (including normal float of outstanding checks) should ordinarily not exceed by any substantial amount the balance required to avoid service charges or the balance required to meet 30 days’ cash expenditures, whichever is larger.

Current funds not required in the checking accounts and all reserve funds must be:

- Carried in interest–bearing accounts in federal credit unions or in federally insured banks or savings institutions, if available locally. The balance in any individual bank or institution may not exceed $100,000.

- Invested in federal government securities registered in the name of the organization and held in a safe deposit box or other secure depository.

Social and recreational funds must be disbursed for the benefit of all employees and should not accumulate over the years.

Employee social and recreational funds are for providing recreational and social activities for the benefit of all postal employees. Expenditures should not be made that will benefit only a single group, organization, or individual.

There are many types of expenditures that may properly be made that will be for the benefit of all the employees. Questions relating to the appropriateness of intended expenditures should be referred to the district manager. Contributions to the following types of projects would be appropriate expenditures for the employee social and recreational committee:

- Gift to an employee or wife of an employee for a new baby, provided the same criteria are used for all employees.

- Retirement gift for an employee, provided the same criteria are used for all employees.

- Expression of sympathy for a death in the immediate family, provided the same criteria are used for all employees.

- An annual party, picnic, or other outing for all employees.

- Seasonal and holiday nonsectarian decorations.

- Sports programs.

- Recreational activities available for all employees.

- Scholarships for children of postal employees, provided the same criteria are used for all employees’ children.

- Microwave ovens, refrigerators, games and recreational equipment for the swing room.

Contributions to the following types of projects would not be appropriate expenditures and should not be made by the employee social and recreational committee:

- Public charities.

- Travel and/or expenses of employee organization official to attend meetings.

- Political campaigns.

- Projects that alter or affect working conditions at postal installations.

A designated member of the committee at each postal installation maintains in a bound ledger a record of all monies received by or disbursed from the fund. (See Exhibit 615.5 for instructions for setting up and maintaining a ledger.)

Pre–numbered checks should be used for disbursements of $10 or more. Smaller disbursements may be made from petty cash. The member of the employee social and recreational committee authorized to sign checks should not be the same person who receives and deposits funds. (See Exhibit 615.5 for instructions.)

A permanent record of all accountable property owned by the employee social and recreational committee should be maintained. Such property includes assets purchased outright, under lease, and on an installment plan, and assets donated. (See Exhibit 615.5 for instructions.)

All supplies on hand should be inventoried by physical count at the end of each fiscal year, or more often if desired. The chairperson of the committee must sign the statement. Records of inventories should be retained for 2 years from date of inventory. (See Exhibit 615.5 for instructions.)

All unpaid bills should be listed at the end of each fiscal year, or more often if desired. All unpaid obligations except those listed in the record of assets should be included. The chairperson of the committee should sign the list. The list should be retained for 2 years. (See Exhibit 615.5 for instructions.)

The employee social and recreational committee at each postal installation must maintain chronological files of any of the following documents or other similar documents pertaining to the operation of the fund:

- Paid invoices showing date paid (with any delivery tickets attached to the related invoice).

- Bank statements and related paid checks.

- Statements from outside vending machine owners covering commissions received by fund or other items.

- Supplies inventory and list of unpaid obligations.

- Financial statements, audit reports, and comments by the district Finance manager.

- Constitution and bylaws, agreements, or regulations covering operations, and minutes of committee meetings.

Exhibit 615.5

Instructions for Keeping Records and Files for the Employee Social and Recreational Committee

Keeping Records and Files for the Employee Social and Recreational Committee

|

Handling the Funds — Appointed Funds Handler

|

Safekeeping

|

Separate funds may not be maintained by stations or branches of one installation.

If the average balance of a fund is…

n decide whether to keep funds in a safe place (such as a safe) or to maintain a bank or credit union account.

n keep all funds except petty cash in a single bank or credit union account.

n make deposits as frequently as necessary, consistent with type and amount of funds received.

n keep excess funds in an interest–bearing account in a federal credit union or federally insured bank or savings institution.

|

Checks

|

The committee member authorized to sign checks should not be the same person who receives and deposits funds.

|

Keeping a Ledger — Appointed Committee Member

|

Permanent Record

|

|

Columns

|

Date Explanation Receipts Disbursements Balance

When the number and type of disbursements, make it practicable to record each of the different types of separate columns, then use additional columns, including one headed Total Disbursements.

|

Entries

|

Do not make an entry when funds are deposited in the bank or credit union because such amounts should have been recorded as a receipt at the time they were received.

|

Balances

|

The balance must always represent the amount of cash on hand in the bank or credit union.

|

Errors

|

If you…

n draw a single line through the incorrect entry.

n insert the correct entry immediately above.

n initial the correction

n record the correction on the next blank line in the column that will bring the ledger into agreement with cash on hand.

n reference the page number and the line being corrected.

|

Keeping Records — Appointed Committee Member

|

Property Assets

|

|

Supplies

|

|

Unpaid Obligations

|

|

Files

|

n Paid invoices, showing date paid, with any delivery tickets attached.

n Bank statements and related paid checks.

n Statements from outside vending machine owners covering commissions received by fund or other items.

n Supplies’ inventory and list of unpaid obligations.

n Financial statements, audit reports, and comments by the district Finance manager.

n Constitution and bylaws, agreements or regulations covering operations, and minutes of committee meetings.

|

All employee social and recreational committees must prepare statements each fiscal year, or more frequently if desired, to show the financial condition of the fund. The committee must complete original forms by typewriter or in ink, using carbon for copies. The committee also must maintain files of all original reports for 2 years from the date prepared.

A statement of receipts and disbursements must be prepared on PS Form 3241, Statement of Receipts and Disbursements (Employee Social and Recreational Funds), Exhibit 615.62. This statement must be signed by the chairperson and treasurer of the social and recreational committee. One copy of the prepared form is retained in committee files, copies are posted on employee bulletin boards, and the original and one copy are sent to the installation head. The installation head must forward one copy of the form to the district Finance manager with the audit report prepared as described in 615.7. Headquarters field units must forward one copy to the vice president and controller of Finance.

Exhibit 615.62

PS Form 3241, Statement of Receipts and Disbursements (Employee Social and Recreational Funds)

Exhibit 615.62 (p. 2)

PS Form 3241, Statement of Receipts and Disbursements (Employee Social and Recreational Funds)

An annual audit must be made of employee social and recreational committee funds. More frequent audits may be made as circumstances dictate.

The head of each installation is required to recommend an independent audit as prescribed in 615.74 when the size and complexity of an operation justifies such action.

The district Finance manager reviews such recommendations and advises installation heads whether an independent audit should be made and may also require that an audit be made irrespective of any recommendations.

When an independent audit is not made, the installation head appoints at least three employees as an audit committee. Normally, the audit committee should be made up of postal system auditors or accounting personnel. This committee may not include any employees responsible for receiving, disbursing, or having custody of funds connected with the vending operations. When three employees are not available, the installation head may make the examination.

When the district Finance manager determines that an independent audit is advisable, this audit must be made in accordance with generally accepted auditing standards by independent certified public accountants, or independent licensed public accountants, certified licensed by a regulatory authority of a state or other political subdivision of the United States. If the installation head has a question as to whether public accountants in the area are certified or licensed by a regulatory authority, he or she must write to the district Finance manager. If public accountants are not licensed or certified, independent audits must be made by certified public accountants.

At a minimum, the audit committee’s review must:

- Determine that the employee social and recreational committee fund is being operated in accordance with prescribed instructions and bylaws.

- Review the immediately preceding audit report for any improper practices previously noted.

- Verify that the records are maintained properly and reflect cash on hand and in the bank. (This verification should be made on an unannounced or surprise basis.)

- Determine that proper percentages for vending machine receipts are being paid and recorded.

- Review all receipts from sources other than vending machines and interest or dividends.

- Review all disbursements for their propriety.

As a minimum, the audit report must include:

- A brief statement of the work performed by the auditor or audit committee.

- Copies of statement of receipts and disbursements as described in 615.62.

- An opinion as to whether the employee social and recreational committee fund is being operated as prescribed by this instruction and committee constitution and bylaws.

- An opinion on the statements prepared by the employee social and recreational committee with any adjustments recommended.

- A detailed list of deviations from instructions, including disbursements for questionable or unauthorized purposes and other deficiencies.

The audit report must be submitted in triplicate to the head of the installation within 60 days after the close of the fiscal year. A copy must be posted on employee bulletin boards. One copy of the report, signed by all members of the audit committee of the outside auditor, must be submitted promptly to the district Finance manager by the installation head.

The installation head is responsible for seeing that proper practices are followed and deficiencies are corrected. Where deficiencies have been noted, the installation head should report to the district manager, by memorandum, the corrective action taken.

The district Finance manager reviews the audit reports to determine that they are complete, and that there is no indication that the committee operations are not in accordance with the prescribed accounting instructions. If a report is considered inadequate, the district Finance manager may request additional information from the installation head or request further examination of the records. The district Finance manager may comment on significant items for the information of the installation head, the district manager, and the committee. Any evidence of deficiencies in internal controls, or financial irregularities of any kind, must be brought to the attention of the installation head.

The Office of Inspector General may periodically audit the employee social and recreational committee operations and funds, and must have complete access to all records and documents pertaining to the committee activities.

The Internal Revenue Service has ruled that employee social and recreational committees that are established and operated in accordance with these regulations are an integral part of the Postal Service, are not subject to federal income taxation, and are not required to file federal income tax returns.

Failure to adhere to the regulations may result in significant income tax liability for the employee and social recreational committee or for individual members of the committee.