|

page 62 of 74 |  |

chapter 3

financial highlights

|

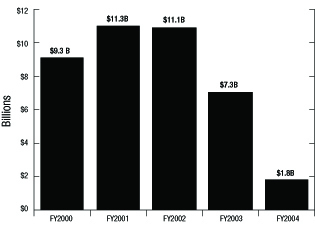

million which it was required to use to repay operating debt. The Postal Service funds its operations chiefly from cash generated from operating revenue. However, unlike other mailers in the private sector, it is not permitted to raise capital through the equity markets, and because the Postal Service is expected to break even over time, it is not expected to retain a substantial amount of retained earnings for extended periods to increase its capital. Consequently its only long-run source of outside capital is through issuing debt obligations. An additional challenge is that the Postal Service, unlike the private sector, is not free to set its own prices for its products and services. The postal rate setting process, established by law, is a complex and lengthy process that can take eighteen months to complete. It cannot be easily adjusted to react to changing market conditions. In 2002 the President and Congress apportioned a total of $762 million for securing the mail and protecting the health and safety of Postal Service employees and customers. At the end of 2004 all of the money has been committed to security related projects. The Postal Service is also required to provide for free and reduced rate mail service for certain groups, and a provision for reimbursement is provided for by law. However, the Postal Service has not been fully reimbursed and is still owed $900 million for this forgone revenue. The amount the Postal Service borrows is largely determined by the difference between its cash flow from operations and its capital cash outlays. Postal Service capital cash outlays are the funds invested back into the business for capital investments in new facilities, new automation equipment, and new services. From 1997 through 2002, Postal Service outlays for capital investment exceeded cash from operations by $5.4 billion, so most of the difference was covered with borrowed funds. From the end of 1997 to the end of 2002, Postal Service debt outstanding with the Department of the Treasury's Federal Financing Bank increased from $5.9 billion to $11.1 billion. In 2003 the Postal Service reduced its debt by $3.8 billion to $7.3 billion and in 2004 by $5.5 billion to $1.8 billion, its lowest level of debt since 1984. The enactment of P. L. 108–18 in 2003 dramatically increased Postal Service cash flow by $6.2 billion in 2003 and 2004. However, under this law, in those two years the Postal Service is required to apply the "savings" realized under the law to debt reduction. The required debt reduction amounted to $3.5 billion in 2003 and an additional $2.7 billion in 2004. |

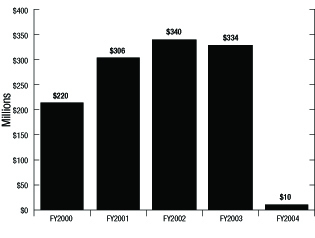

The Postal Service undertook financing actions in 2003 that laid the foundation for financial gains in 2004. In 2003 the Postal Service completely overhauled its debt portfolio, paying off all of long-term debt obligations and replacing most of them with short-term debt that would be retired during the course of 2004. As a result of the overhaul, the Postal Service benefited from both lower interest rates on short-term debt and also from the flexibility to repay debt with available cash on a daily basis. A major benefit was the reduction in the interest expense it pays to the Federal Financing Bank. Reflecting this change, interest expense on borrowings, net of capitalized interest, was $10 million in 2004, the lowest since 1972, versus $334 million in 2003, and Figure 3-4 Debt at Fiscal Year End

Figure 3-5 Interest Expense on Borrowings

|