|

page 30 of 66 |  |

Financial review

Part II

|

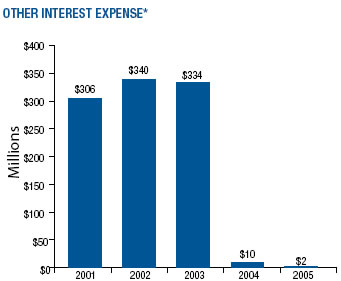

*Other interest expense excludes interest on deferred retirement |

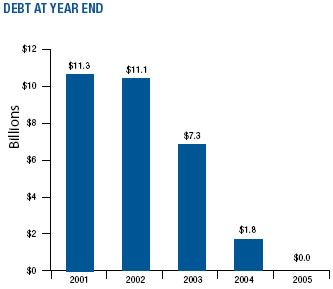

Finance Debt As an independent establishment of the executive branch of the United States government, we receive no tax dollars for our operations. We are self supporting, and have not received a public service appropriation since 1982. The last time we received any substantial contribution of capital from the U.S. government was in calendar years 1976 and 1977, when we received two $500 million payments which we were required to use to repay operating debt. We fund our operations chiefly from cash generated from operating revenue. However, unlike companies in the private sector, we are not permitted to raise capital through the equity markets. Consequently our only source of outside capital is through securing debt obligations. An additional challenge is that we, unlike the private sector, are not free to set our own prices for our products and services. The postal rate setting process has been a complex and lengthy process in the past. The uncertainty created by this process influences our cash management strategy. The amount we borrow is largely determined by the difference between our cash flow from operations and our capital cash outlays. Our capital cash outlays are the funds invested back into the business for capital investments in new facilities, new automation equipment, and new services. At the beginning of 2003 our debt stood at $11.1 billion. During that year, we reduced our debt by $3.8 billion and, in 2004 by $5.5 billion. Cash flow from operations in 2005 enabled the repayment of the remaining debt. This is the first time since postal reorganization that we have ended the year with no debt obligations outstanding. We undertook debt refinancing actions in 2003 that laid the foundation for financial gains in 2004 and 2005. In 2003, we completely overhauled our debt portfolio, paying off all of long-term debt obligations and replacing most of them with short-term debt that would be retired during the course of 2004. As a result of the overhaul, we benefited from both lower interest rates on short-term debt and also from the flexibility to repay debt with available cash on a daily basis. A major benefit was the reduction in the interest expense payable to the Federal Financing Bank. Reflecting this change, interest expense on borrowings in 2005, was the lowest since postal reorganization. This meant that while we paid an average of $327 million in Interest expense from 2001-2003 we were able to virtually eliminate interest expense in 2004 and 2005. |