|

U-ni-ver-sal adj [from universum

the universe] 1: comprehensively broad and versatile

without limit or exception 2: combine that with service

and you're talking about the mission of the United States Postal Service

— affordable, universal service for every American.

Our capital plan for the future calls for aggressive cost

management by developing and deploying new automation and mechanization

equipment that will increase our operating efficiency. We estimate our

total capital commitment plan for 2003 at $2.5 billion. We will continue

to concentrate on maintaining such infrastructure as facilities, vehicles

and systems, as well as return on investment projects. Under this plan,

we will make investments in programs that reduce work hours in our distribution,

processing and delivery operations. A prime example of this type of investment

is Postal Automated Redirection System (PARS) approved by the Board of

Governors in 2002. PARS will identify and intercept letters that should

be forwarded during the initial handling and automatically redirect them

to the new address. Each year we process more than 43 million change-of-address

orders and over 5 billion pieces of mail that must be either forwarded,

returned to sender or handled alternatively. The total cost attributed

to this activity exceeds $1.5 billion annually. PARS technology will help

us capture cost savings by reducing labor and the time required for delivery.

With the exception of mail forwarding, there are no new major automated

equipment initiatives left for letter mail. We will focus on flat mail

processing, including the Flats Optical Character Reader, Flats Identification

Code Sorter and the Flats Feeder Enhancement Program. We expect this focus

will be as successful as our efforts in reducing costs for letter mail

processing.

In 2001, our facility-related investments were limited to those that addressed

emergency, safety and legal issues; modifications to ongoing construction;

planning funds for a small number of major projects and opportunities

for revenue generation or significant savings. In 2002, we expanded these

criteria to address high growth areas, facility obsolescence and necessary

maintenance of our real property assets. We review projects meeting these

criteria on a case-by-case basis.

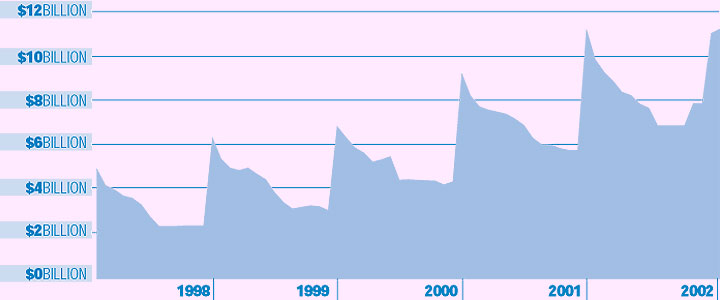

From 1997 through 2001, our capital cash outlays exceeded cash flow from

operations by $5.3 billion, so we covered the difference with borrowed

funds. Our debt outstanding with the Department of the Treasury’s Federal

Financing Bank increased by $5.4 billion during that period. This year,

however, we were able to reverse the trend of increasing debt each year.

Debt outstanding at the end of the year was $11.1 billion, a decrease

of $200 million compared to 2001.

Our debt balance at the end of the year represents our highest level of

debt for the year because, while we accrue our expenses for workers’ compensation

and deferred retirement benefits throughout the year, we make the actual

payments in late September. This year we paid $4.7 billion, including

$787 million for workers’ compensation and $3.9 billion for the Civil

Service Retirement System (CSRS) deferred retirement costs and cost of

living adjustments (COLAs) for retirees. Our cash flow throughout the

year was sufficiently strong to reduce debt from the prior year-end level.

We have debt financing flexibility and can manage the fluctuations in

our debt during the year by actively managing our credit lines. However,

just as our debt balance at year-end has increased in recent years, so

has our average debt level. The graph of our debt during the year illustrates

this point well, showing that the peaks were getting higher each year.

For 2002, our average outstanding debt during the year was less than the

prior year-end balance but increased 20.3%, or $1.3 billion, to $7.7 billion.

Our interest expense totaled $340 million in 2002, compared to $306 million

in 2001. Managing cash and debt on a daily basis is one of the means we

use to minimize annual interest expense.

|

|

|